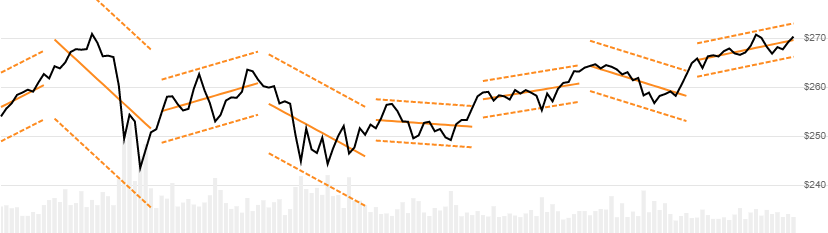

Standard Deviation Channels

Standard Deviation Channels are prices ranges based on an linear regression centerline and standard deviations band widths. [Discuss] 💬

// C# usage syntax

IEnumerable<StdDevChannelsResult> results =

quotes.GetStdDevChannels(lookbackPeriods, stdDeviations);

Parameters

lookbackPeriods int - Size (N) of the evaluation window. Must be null or greater than 1 to calculate. A null value will produce a full quotes evaluation window (see below). Default is 20.

stdDeviations double - Width of bands. Standard deviations (D) from the regression line. Must be greater than 0. Default is 2.

Historical quotes requirements

You must have at least N periods of quotes to cover the warmup periods.

quotes is a collection of generic TQuote historical price quotes. It should have a consistent frequency (day, hour, minute, etc). See the Guide for more information.

Response

IEnumerable<StdDevChannelsResult>

- This method returns a time series of all available indicator values for the

quotesprovided. - It always returns the same number of elements as there are in the historical quotes.

- It does not return a single incremental indicator value.

- Up to

N-1periods will havenullvalues since there’s not enough data to calculate.

👉 Repaint warning: Historical results are a function of the current period window position and will fluctuate over time. Recommended for visualization; not recommended for backtesting.

StdDevChannelsResult

Date DateTime - Date from evaluated TQuote

Centerline double - Linear regression line (center line)

UpperChannel double - Upper line is D standard deviations above the center line

LowerChannel double - Lower line is D standard deviations below the center line

BreakPoint bool - Helper information. Indicates first point in new window.

Utilities

See Utilities and helpers for more information.

Alternative depiction for full quotes variant

If you specify null for the lookbackPeriods, you will get a regression line over the entire provided quotes.

Chaining

This indicator may be generated from any chain-enabled indicator or method.

// example

var results = quotesEval

.Use(CandlePart.HL2)

.GetStdDevChannels(..);

Results cannot be further chained with additional transforms.