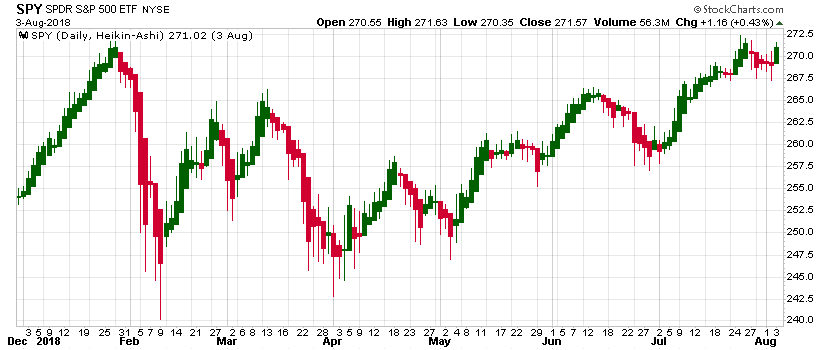

Heikin-Ashi

Created by Munehisa Homma, Heikin-Ashi is a modified candlestick pattern based on prior period prices for smoothing. [Discuss] 💬

// C# usage syntax

IEnumerable<HeikinAshiResult> results =

quotes.GetHeikinAshi();

Historical quotes requirements

You must have at least two periods of quotes to cover the warmup periods; however, more is typically provided since this is a chartable candlestick pattern.

quotes is a collection of generic TQuote historical price quotes. It should have a consistent frequency (day, hour, minute, etc). See the Guide for more information.

Response

IEnumerable<HeikinAshiResult>

- This method returns a time series of all available indicator values for the

quotesprovided. - It always returns the same number of elements as there are in the historical quotes.

- It does not return a single incremental indicator value.

HeikinAshiResultis based onIQuote, so it can be used as a direct replacement forquotes.

HeikinAshiResult

Date DateTime - Date from evaluated TQuote

Open decimal - Modified open price

High decimal - Modified high price

Low decimal - Modified low price

Close decimal - Modified close price

Volume decimal - Volume (same as quotes)

Utilities

- .Find(lookupDate)

- .RemoveWarmupPeriods(qty)

-

.ToQuotes() to convert to a

Quotecollection. Example:IEnumerable<Quote> results = quotes .GetHeikinAshi() .ToQuotes();

See Utilities and helpers for more information.

Chaining

Results are based in IQuote and can be further used in any indicator.

// example

var results = quotes

.GetHeikinAshi(..)

.GetRsi(..);

This indicator must be generated from quotes and cannot be generated from results of another chain-enabled indicator or method.